- انطلاق أولى جلسات امتحان شهادة الدراسة الثانوية العامة لعام 2026 (الصف الثاني عشر – جيل 2008) الخميس ، وتستمر حتى السبت 18 تموز المقبل

- وزير الداخلية، مازن الفراية، يجري زيارة تفقدية مفاجئة إلى جسر الملك حسين، هي الثانية خلال أسبوع

- الهيئة الخيرية الأردنية الهاشمية، تسيّر الخميس، القافلة التاسعة من المساعدات الإنسانية إلى الجمهورية اللبنانية

- وفاة طفل يبلغ من العمر 9 سنوات غرقاً في أحد الشاليهات بمحافظة جرش، وفق مصدر طبي في مستشفى جرش الحكومي

- ارتفاع حصيلة ضحايا زلزالين قويين ضربا فنزويلا، مساء الأربعاء، إلى 32 قتيلا على الأقل وأكثر من 700 جريح

- جيش الاحتلال الإسرائيلي يعلن مقتل متعاقد في "حادث عملياتي" في غزة الأربعاء

- يكون الطقس، الخميس، صيفيًا معتدل الحرارة في المرتفعات الجبلية والسهول، وحارًا نسبيًا في مناطق البادية، وحارًا في الأغوار والبحر الميت والعقبة

Why did Capital Bank pay the lowest tax rate among banks over the past five years

08/04/2025 - 13:13

Capital Bank of Jordan just turned 30 years old. ?

For that occasion, the CEO of the bank sat down with the economics editors of Al Rai newspaper. The interview (full link here) went exactly as one would imagine: a corporate propaganda piece with gentle questions from the interviewer.

This is the kind of soft journalism that I don’t like in Jordan where they miss the opportunity to ask the really hard questions that are on (almost) everybody’s mind. I understand that some journalists in general don’t like to upset people but that particular interview didn't make sense. It felt like it would fit better in those out of circulation (and somewhat missed) finance magazines like Jordan Business or Venture Magazine. I mean it’s not like the bank is the largest corporate subscriber to Al Rai, its largest lender1, or its largest sponsor and advertiser booking the front page on a daily basis. Al Rai’s largest source of revenue is government tender ads, court case announcements, and obituaries. Therefore the newspaper is free to scrutinise anyone without fear of repercussion and/or losing any ad business. Fortunately (or unfortunately), it is not in our culture to do so - at least on paper.

{kind=link}

That’s why Substack exists - the last bastion of free (and responsible) expression. And if I were personally interviewing the bank, I would have asked a series of very different questions and the most important one, which I think would be important to a lot of people, is:

Why did Capital Bank pay the lowest tax rate amongst banks for the past 5 years?

The tax rate for banks is 35% + a 3% contribution which makes it a total of 38% (the highest compared to all other sectors in the country).

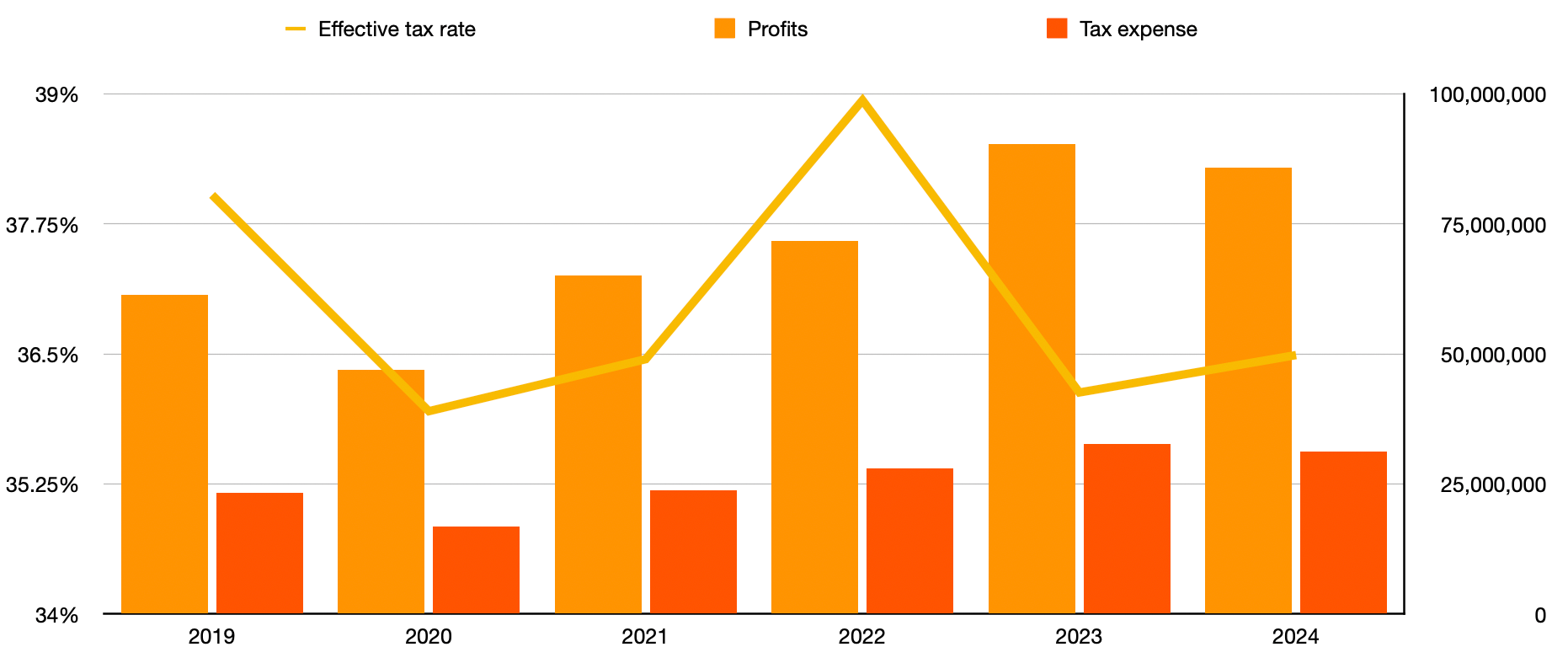

Capital Bank’s profits and tax payments (RHS) with the tax rate (LHS). Source: Capital Bank’s financial statements

Capital Bank had averaged an effective tax rate of 14% for the past 5 years. I personally paid a higher tax rate than the bank itself!! (and my rate was based on my gross income).

In comparison, all other banks paid the correct tax rate (or at least >25% depending on the year).

As an example2, here is Bank Al Etihad’s tax rate (it averaged around 36% for the same period).

{kind=link}

Bank al Etihad’s profits and tax rate. Source: Etihad’s financial statements.

Now is that fair? Of course not. It’s not fair to the average tax paying citizen, to the other banks, and most importantly it is not fair to the tax department itself (i.e. the treasury).

Had Capital Bank paid let’s say on average 35% tax on its profits in the last 5 years, it would owe on top of what it had already paid: 116 million JODs. That’s more than what it paid in total in the 6 years.

Now this question of why Capital paid such a low rate lets one speculate:

i-did the bank get a special agreement from the tax department?

ii-did the bank find a loophole in the tax code - like allocating to their Dubai DFIC registered subsidiary Capital Investments the 2 billion government bonds and not pay capital gains tax?

iii-or worse, is the bank manipulating the books?

No, it’s actually none of the above. With very strict banking and auditing rules implemented in Jordan, there is no way for a bank to do such a mistake.

The Real Reason: IFRS 10

In fact the answer is very straightforward and lies in the way the International Financial Reporting Standards works (mainly IFRS 10) and Capital Bank’s subsidiary in neighbouring Iraq:

Capital Bank owns 2/3 of the National Bank of Iraq (NBI) - it controls 61.85% of the bank.

According to IFRS 10, Capital Bank is allowed to combine both its own revenue in Jordan and that of Iraq (not 61.85% of Iraqi revenue, but 100%).

The income tax rate for banks in Iraq is 15% unlike Jordan’s 38%,

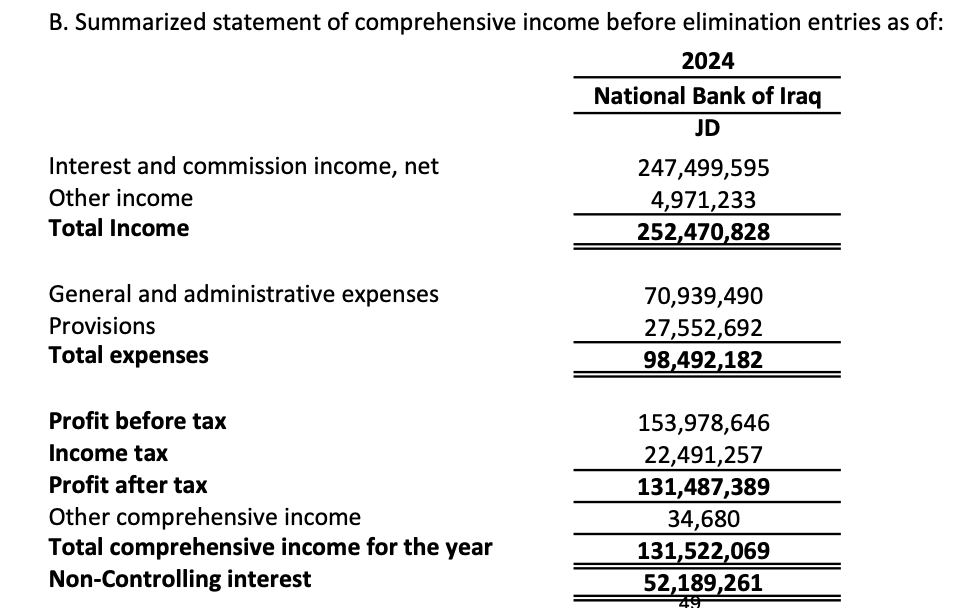

Page 49 of the bank’s statement. Link

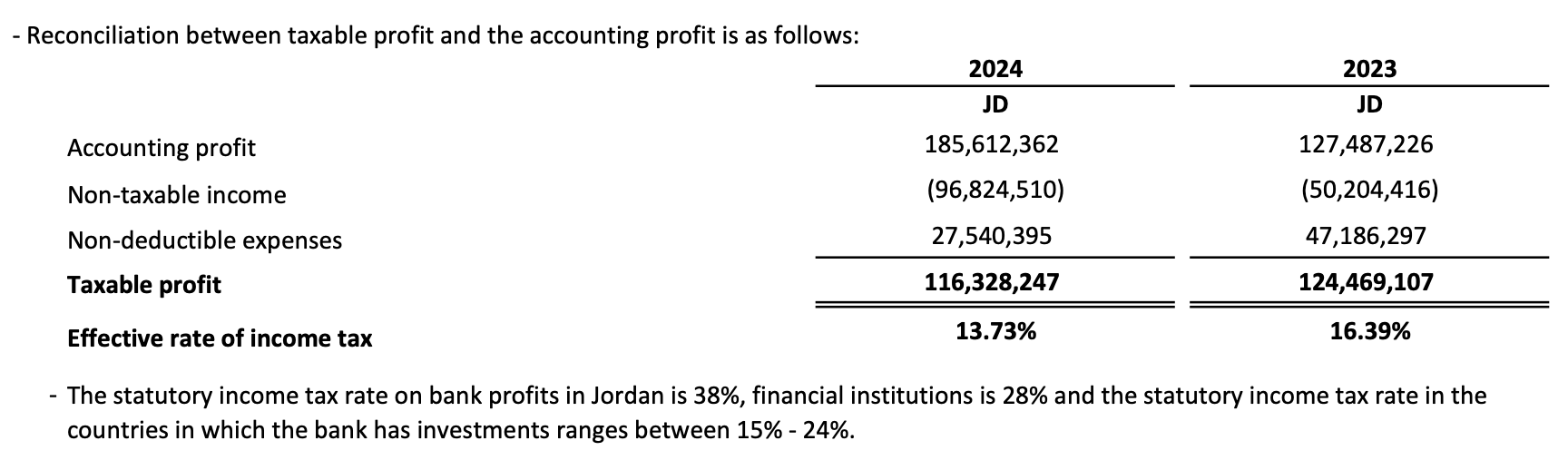

NBI made a profit before tax of ~154 million JODs (and paid 22.5 million JODs of income tax - at the correct rate of 15%). Looking at the section 21 of the statement below, we can clearly see the reconciliation of accounting profit and tax profit with the non-taxable income of 96 million JODs which is basically 61.85% of the 154 million profit made by NBI. Therefore, there was no wrongdoing done by anyone.

Page 47 of the statement

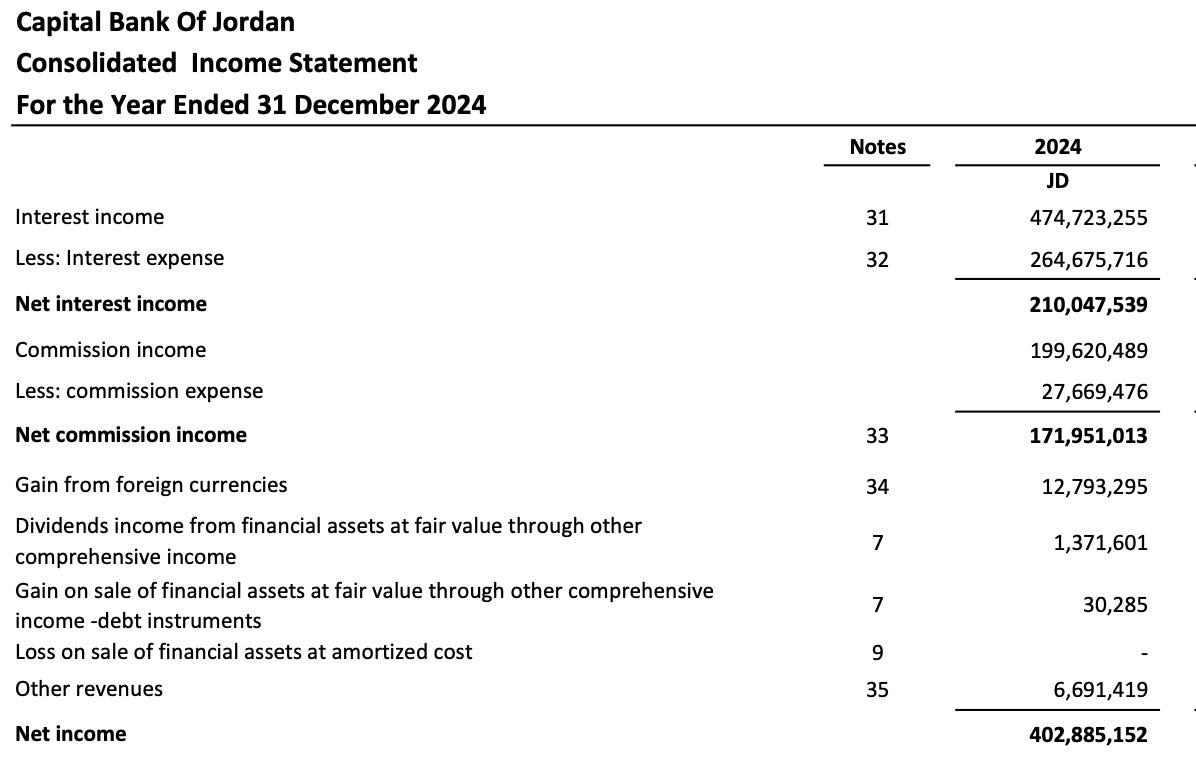

But, hang on, let’s go back to the first page and look at the ‘group’s’ total income: the consolidated statement shows that the total net income for 2024 was 402 million JODs (210 million net interest income and 170 million commissions and transfer fees, one of the highest among other banks).

This basically means that Capital Bank Jordan alone (without NBI) realised a net income of 402 - 252 = 150 million JODs. This number is much lower than that of its Iraqi counterpart despite Capital having absorbed 2 local banks in the last few years.

Conclusion: The Iraqi sub, which was once a liability to Capital, is proving to be a main driver for growth and the reason why the effective tax rate seems so low at first.

Capital Bank is not the largest lender per Al Rai’s last financial statement. In fact Capital Bank sequestered the expensive printing press on the airport road: https://jordanfinance.substack.com/p/who-will-save-al-rai/comments. In the link is also a brief analysis of how Al Rai lost its way, financially speaking.

{kind=link}

The tax rate for the biggest companies in the Amman Stock Exchange can be found in the table in this post (by doing a quick calculation and works best on desktop browsers):

{kind=link}